How to Calculate Home Loan EMI (Complete Guide)

Buying a home is one of the biggest financial decisions in life. While it’s an emotional milestone, it also requires careful financial planning. One of the most important things you must understand before taking a loan is your EMI (Equated Monthly Installment).

If you don’t calculate it properly, your dream home can turn into a financial burden.

What is Home Loan EMI?

EMI (Equated Monthly Installment) is the fixed amount you pay every month to repay your home loan.

It consists of two parts:

- Principal → The amount you borrowed

- Interest → The cost of borrowing money

In the early years, most of your EMI goes toward interest

Later, more goes toward principal repayment

This gradual shift is called amortization.

🧠 Why EMI is Important

Understanding EMI helps you:

- Plan your monthly budget

- Avoid financial stress

- Compare loan options

- Choose the right tenure

- Manage long-term finances

Simply put: EMI decides whether your loan is affordable or not

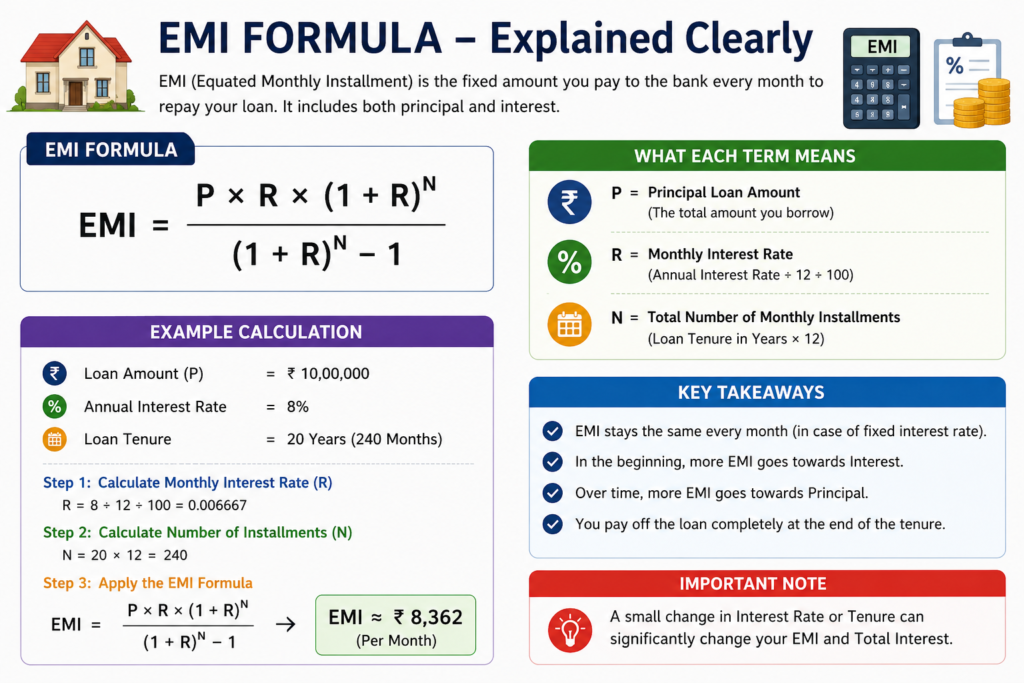

Home Loan EMI Formula

The EMI formula used by all banks is:EMI=(1+R)N−1P×R×(1+R)N

Where:

- P = Loan amount

- R = Monthly interest rate (Annual Rate ÷ 12 ÷ 100)

- N = Loan tenure in months

Here is another andeasy visualization

Example Calculation

Let’s understand with a real example:

- Loan Amount = $100,000

- Interest Rate = 8% annually

- Tenure = 20 years (240 months)

Step 1: Monthly Interest Rate

R=12×1008=0.00667

Step 2: Apply Formula

EMI ≈ $836 per month

Total Payment Insight

- Total Payment = $836 × 240 = $200,640

- Total Interest = $100,640

You are paying almost double due to interest.

EMI Amortization Explained

| Period | Interest Portion | Principal Portion |

|---|---|---|

| Early Years | High | Low |

| Mid Years | Balanced | Balanced |

| Final Years | Low | High |

👉 This is why early prepayment saves a lot of money

Easy Method: Use an EMI Calculator

Manual calculation can be complex. Using an online EMI calculator is better.

Benefits:

✔ Instant results

✔ No calculation errors

✔ Shows total interest

✔ Displays amortization schedule

👉 If you’re building your real estate website, adding an EMI calculator will:

- Increase user engagement

- Improve SEO

- Help with AdSense approval

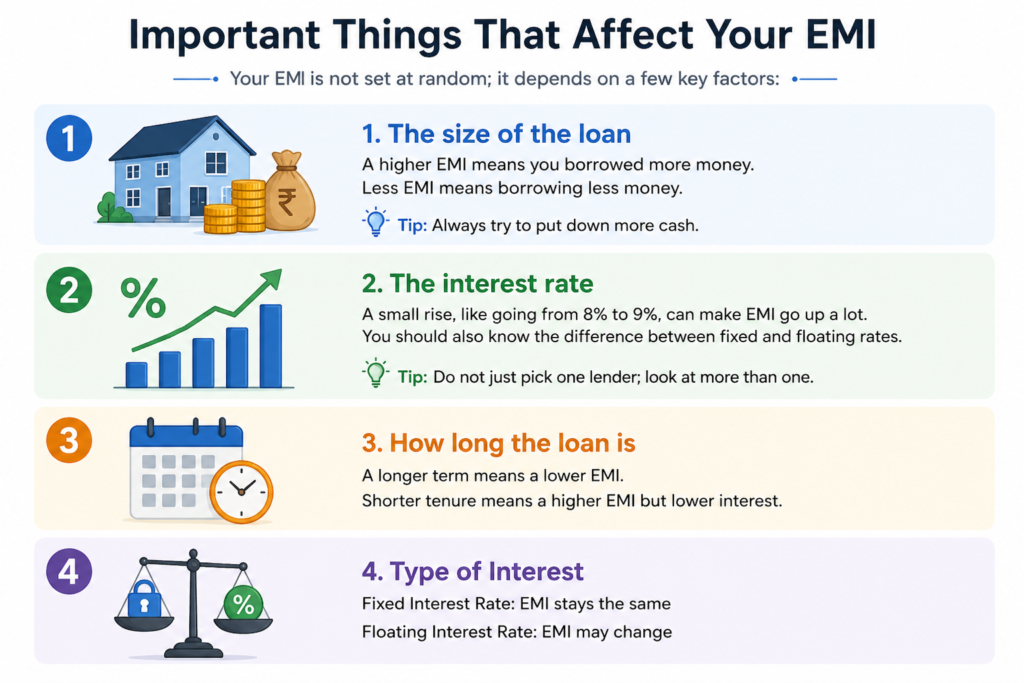

Factors That Affect EMI

1. Loan Amount

- Higher loan → Higher EMI

- Lower loan → Lower EMI

👉 Tip: Increase down payment

2. Interest Rate

Even a small change matters:

- 8% → Lower EMI

- 9% → Significantly higher EMI

👉 Tip: Compare multiple lenders

3. Loan Tenure

| Tenure | EMI | Total Interest |

|---|---|---|

| Long | Low | High |

| Short | High | Low |

Interest Type

- Fixed Rate → EMI stays same

- Floating Rate → EMI may change

Smart Ways to Reduce EMI

- Increase down payment

- Choose longer tenure (carefully)

- Compare interest rates

- Make early repayments

- Improve credit score

- Transfer balance to lower rate bank

EMI vs Total Cost (Common Mistake)

Many people focus only on low EMI.

But you should focus on:

- Total interest paid

- Total repayment amount

Slightly higher EMI can save you lakhs in the long run.

Advanced Insight

Even a 1% increase in interest rate can significantly increase EMI and total cost.

Useful Financial Tools

You should also use:

- Loan Calculator

- Mortgage Calculator

- ROI Calculator

- Savings Calculator

These help you make better financial decisions.

❓ FAQs

Q1: Is EMI always fixed?

✔ Yes (fixed rate loans)

❌ No (floating rate loans)

Q2: Can EMI increase?

✔ Yes, in floating interest loans

Q3: What happens if EMI is missed?

- Penalty charges

- Credit score damage

- Legal action (in severe cases)

Q4: Are online EMI calculators accurate?

✔ Yes, they use standard banking formulas

Q5: Short tenure or low EMI?

- Low income → Choose low EMI

- Stable income → Choose shorter tenure

Common Mistakes to Avoid

❌ Not calculating EMI before loan

❌ Ignoring total interest cost

❌ Choosing longest tenure blindly

❌ Not comparing lenders

❌ Ignoring prepayment options

Final Thoughts

Calculating your EMI is not just math—it’s a financial planning tool.

Before taking a home loan:

✔ Calculate EMI

✔ Compare options

✔ Plan repayment

✔ Think long-term

👉 A well-planned EMI keeps your dream home stress-free.

Disclaimer

This article is for educational purposes only. Interest rates and loan terms may vary. Always consult your bank or financial advisor before making decisions.

If you liked our blog you can connect by our social profile :

Follow us for real estate tips, tools, and updates

If you liked our blog you can connect by our social profile :

Follow us for real estate tips, tools, and updates