EMI vs Salary: How Much Loan Can You Afford?

Buying a house is one of the most important financial choices you’ll ever make. It’s a big emotional step, but you need to think about it carefully because it’s a long-term financial commitment. One of the most important things for every buyer to think about is how much they can really borrow based on how much they make.

You might not think this question is important, but it is. People borrow money based on what banks say they can pay back, not what they can really pay back. This means they have to deal with high EMIs, not having enough money saved up, and money problems.

Knowing how your salary and EMI (Equated Monthly Installment) are linked is the best way to make a smart choice without getting too stressed.

Before you do anything else, use our Home Loan Interest Calculator to figure out how much your monthly payment will be.

What is EMI, and why is it important to get paid?

You pay the same amount on your home loan every month. This is your monthly payment, or EMI. It has:

- The principal is the total amount of money you owe.

- You have to pay interest on any money you borrow.

When you make an EMI payment, the amount you owe on your loan goes down.

Here are some reasons why your pay matters:

- You pay EMI with the money you make each month.

- Your money has an effect on your life.

- Your savings and plans for the future will change.

If your EMI is too high compared to what you earn, it can lead to:

- Pressure to pay your bills

- Every day, it’s hard to remember how much things cost

- Not as good at saving cash

- More likely to not pay back a loan

Read our full guide on How to Calculate Home Loan EMI to find out more about this.

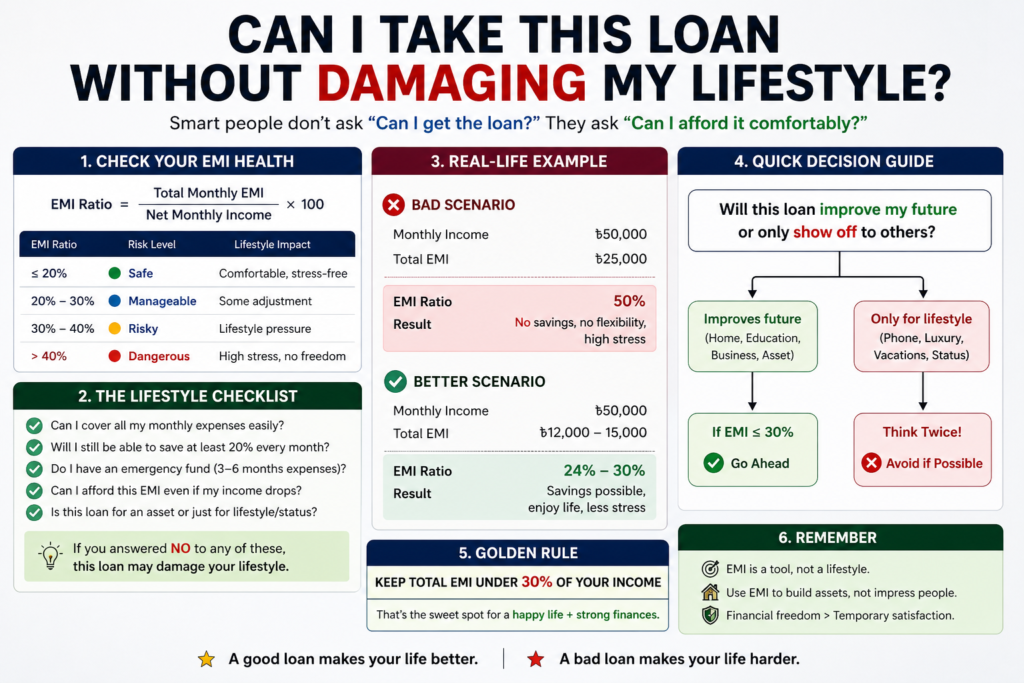

The Best Salary-to-EMI Ratio

A lot of banks and financial experts say this:

👉 Your EMI should be 30% to 40% of your monthly income.

This is how simple it is to stay safe in this case.

For instance:

- $1,000 every month

- Safe EMI: $300 to $400

This range makes sure that you:

- Can keep track of how much you spend every day

- Set aside some money for emergencies

- Keep on living well

What This Ratio Means

This ratio can help you:

- Don’t let money get in the way

- Keep your credit score up

- Make sure that people return the money they borrowed

- Find a way to save money while also spending it

- Make plans for your investments ahead of time

If you don’t follow this rule, you could end up in a lot of debt.

How banks choose who can borrow money

Banks don’t just choose a loan amount at random. They look at a lot of things before they give you the money.

Things that banks care about

- Getting paid every month

- Current EMIs

- Your age, job security, credit score, and the length of the loan all matter

Banks usually find out the FOIR, which stands for Fixed Obligation to Income Ratio.

FOIR is the number of EMIs you have to pay every month divided by your monthly income.

Most banks should have a FOIR between 40% and 50%.

You can find out how much money you can borrow with our Loan Eligibility Calculator and you will find Best Loan Service For Job Holder in USA , Its Called CNBC

How much cash can you get?

Let’s get to the point.

You can only borrow as much as you can easily pay back in EMI.

How to Think:

- Find out how much money you make every month

- Take out between 30% and 40% of it as an EMI

- Look at the EMI to see how much the loan is

For example:

- $2,000 every month

- Safe EMI: $800 (40%)

This EMI:

- With an 8% interest rate for 20 years

👉 You can borrow more than one hundred thousand dollars.

Our Simple Interest Calculator will give you the most accurate results.

How to Get a Loan with a Lower Interest Rate

Here are some important things that affect how much money you can borrow:

1. Make payments every month

You can get more loans if you make more money because you can pay back more each month.

2. Loans or EMIs that are already in place

If you already have:

- Take out a loan for yourself

- Money for a car

- Credit card debt

It will be harder for you to borrow money.

3. The Interest Rate

A small change in the interest rate can have a big effect on your EMI.

- The EMI is lower when the interest rate is lower, which makes it cheaper

- When you have less money to spend, your EMIs go up, which means a higher interest rate

4. How long the loan is

The loan’s term is very important:

- A longer term means a lower EMI

- If your term is shorter, your EMI will be higher, but your interest will be lower

5. Your credit rating

A higher credit score means:

- Makes it more likely that you will get a loan

- Reduces the interest rates on loans

The Fixed vs Variable Loan Calculator will help you understand your options.

EMI vs. Salary: Examples from Real Life

Let’s talk about the different ways to pay:

Case 1: Low Income

- Pay: $500

- Safe EMI: $150

👉 There will be a limit on the amount of the loan. You need to give it some serious thought.

Case 2: Middle Income

- Pay: $1,500

- Safe EMI: $450 to $600

👉 Not too expensive

👉 Good chance of getting a loan

Case 3: High Income

- Pay: $5,000

- Safe EMI: $1,500 to $2,000

👉 More loan options give you more freedom

Our Rent vs Buy Calculator can help you figure out if buying is the best option for you.

Things You Should Think About That Will Cost You

You shouldn’t only think about EMI.

But there are also other costs, like:

- Taxes on property

- Costs for upkeep

- Insurance

- Registering it

- Prices for getting legal help

These can really change how much money you have to spend each month.

How to Handle EMI Based on Your Income

Here are some tried-and-true ways to keep your bills down:

Increase the Down Payment

The more you pay ahead of time:

- The less you take out

- The lower your EMI will be

Choose the Right Tenure

- Longer term → Lower EMI

- Shorter term → Higher EMI but less interest

Choose what makes you happy.

Improve Your Credit Score

A high credit score can help you a lot:

- You don’t have to pay as much in interest

Avoid Multiple Loans

Too many EMIs make it harder to pay your bills and make your money problems worse.

Plan for Future Costs

Think about:

- Costs for the family

- Medical emergencies

- Education

Pay off your loan early

Pay less if you can to lower:

- The total amount of interest paid over the life of the loan

EMI vs. Lifestyle Balance

One of the most common things people do wrong is:

👉 Getting as much cash as they can

But just because you can buy it doesn’t mean you can afford it.

You should ask:

- Can I put money aside after the EMI?

- Can I handle emergencies?

- Is it okay for me to keep living like this?

👉 Every time, pick comfort over the most money you can borrow.

What Happens When EMI Is High Over Time

A high EMI can have a big impact on many areas of your life:

- Not as much money saved

- More pressure

- Fewer chances to invest

On the other hand, a balanced EMI:

- It helps you feel better

- It helps you earn money

- It helps you stay financially secure

Tools That Help You to Find Out How Much Loan Can You Afford!

Here are some tools to help you make better money decisions:

These tools help you plan well by getting you to think about different situations.

Things You Shouldn’t Do

Things that people do all the time that you shouldn’t do:

❌ Only getting a loan if the bank says yes

❌ Not thinking about how much interest it will cost in the end

❌ Not looking at other lenders

❌ Choosing the longest term without thinking about it

❌ Not having any money saved up for emergencies

❌ Not thinking about how much things will cost later

Questions That Come Up Often (FAQ)

Q1: Can I get an EMI that is half of what I make?

It’s a bad idea and also risky. Keep it between 30% and 40%.

Q2: Does how much money you make affect how likely you are to get a loan?

Yes, if you have a higher income, you are more likely to get a loan.

Q3: What if I get a better job later?

You can:

- Increase EMI

- Pay back the loan early

- Reduce tenure

Q4: Is it still possible for me to get a loan if I don’t make a lot of money?

Yes, but your loan will be for less money.

Q5: Should I choose a short term loan or one with a low monthly payment?

- More comfort with less EMI

- Less interest with shorter tenure

Final Thoughts

The first step to making smart financial plans is knowing how to handle your salary and EMI.

Before you get a mortgage:

✔ Learn how much you can spend

✔ Know how much you can pay each month

✔ Plan how you’ll spend your money over time

✔ Don’t borrow too much money

A well-planned loan will help you keep track of your money and give you peace of mind.

⚠️ Watch out

The only thing this article is meant to do is give you information. There are different rules for different lenders and places about who can borrow money, how much interest they charge, and what those rules are. Always talk to your bank or financial advisor before making any decisions about money.

If you liked our blog you can connect by our social profile :

Follow us for real estate tips, tools, and updates