How Mortgage Works: A Beginner’s Complete Guide

Buying a house is one of the greatest financial choices that most individuals will ever make. Knowing how mortgage works will enable you to avoid expensive errors and choose the proper loan for your future.

If this is your first time purchasing a property in the US, UK or Europe, financing might be difficult. Interest rates, lending conditions, deposits and monthly installments are daunting. But once you have the fundamentals down it’s a lot less challenging.

This tutorial breaks out mortgages in plain English, covering everything from kinds of mortgage to repayment plans, suggestions for borrowers and common errors to avoid.

Table of Contents

- What’s a mortgage?

- How Does a Mortgage Work

- Reasons to Learn About Home Loans

- Mortgage Types

- Major Costs of a Mortgage Explained

- How To Get a Mortgage

- Key Tips Managing Your Mortgage

- Biggest Mortgage Mistakes to Avoid

- Biggest Mortgage Tools & Solutions

- Mortgage Comparison Table

- Conclusion

What Is a Mortgage Loan?

A mortgage is a loan used to acquire real estate or property. You borrow money from the bank or any other lender to buy a house and then pay that money back over time with interest.

The loan is secured by the property. That means if the borrower defaults on the mortgage, the lender may seize the property via foreclosure.

Most common ways mortgages are used for:

- Sell Homes

- Purchasing a Flat

- Clearing old accounts

- Real Estate Investing

- Commercial Property

The length of time for most mortgages ranges from 15 to 30 years, depending on the contract terms.

For official mortgage information, you can also check:

How a Mortgage Works

To see how mortgages function, you have to grasp the connection between the borrower and the lender.

The standard technique is as follows:

- You choose a property.

- You make a deposit or a payment.

- The remainder is covered by the lender.

- You pay the loan each month.

- Payment of principle plus interest.

Principal and Interest

Principal

Principal is the money that you withdraw from the lender.

For example:

- House price: $300,000

- $60,000 down payment

- Mortgage: $240,000

The primary in this situation is $240,000.

Interest

Interest is the price of borrowing money. Interest is a percentage that lenders charge on the amount you borrow.

Greater interest equals greater monthly payments.

You can compare current mortgage interest rates from:

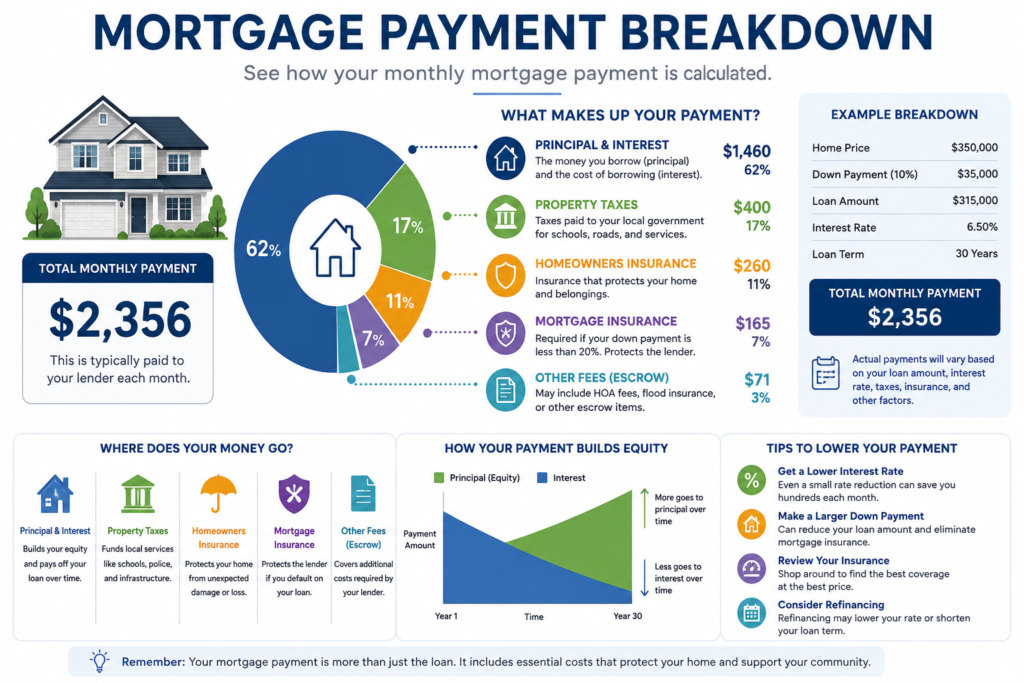

Monthly Mortgage Payment

Mortgage payments typically include:

- Interest Loan sum

- Property Taxes

- Household insurance

- Mortgage insurance (if any)

These combined payments are sometimes commonly referred to as PITI:

- Principal

- Taxes

- Insurance

- Interest

Why You Need To Know About Mortgages

Knowing how mortgages operate will lead you to make better choices with your money.

Budget Better

You can calculate out monthly payments and not borrow more than you can afford.

Lower Financial Risk

You may avoid excessive interest loans and hidden costs if you know the conditions of the mortgage.

Improved Credit Performance

Over time, making timely and responsible mortgage payments helps boost your credit.

Long-Run Financial Stability

Owning a home is a great way to develop wealth, and a good mortgage is a great way to do it.

Types of Mortgage

Various forms of mortgages are suitable for various financial conditions.

Mortgage – Fixed Rate

A fixed-rate mortgage has an interest rate which stays the same throughout the term of the loan.

Benefits

- Regular fixed payments

- Easier to plan your budget

- Protection against increasing interest rates

Best For

For those who plan to stay in one home for many years.

Adjustable Rate Mortgages (ARMs)

A variable-rate mortgage has an interest rate that fluctuates over time.

Advantages

- Lowered entrance costs

- Potential savings if rates drop

Risks

- Payments may be a surprise

Ideal For

Risk takers to accept a financial risk.

Interest-only Mortgage

The borrower only pays interest for a fixed term.

Benefits

- Less down payment

Risks

- No principle reduction on the loan

- Increased payouts in the future

FHA and Government Backed Loans

Some nations have government guaranteed mortgage plans.

Often these help:

- First-time buyers

- Families with little income

- Buyers with a lower credit rating

Breaking Down Big Mortgage Costs

Many debtors look simply at the monthly payment. But there are additional fees of a mortgage.

Payment

It is the first payment towards the acquisition of the property.

Typical ranges are:

- US: 3%-20%

- United Kingdom: 5-20%

- Europe: Depends on the nation

Interest Rate

The lender’s rate of charge.

A little variation in rates might make or lose you thousands of dollars over time.

Expenses of Settlement

These may consist of:

- Legal expenses

- Property appraisal fees

- Loan origination fees

- Taxes

- Mortgage insurance

Some lenders may want insurance if your down payment is minimal.

And this is to the lender’s protection, not the borrower’s.

How to Get a Mortgage

Mortgage applications are typically a uniform procedure.

1. Check Your Credit Score

A higher credit score might help you qualify for reduced interest rates.

You can monitor your credit score using:

2. Calculate your Budget

Use online mortgage calculators to see what you can afford to pay each month.

Helpful tools:

3. Comparison Shopping

Different lenders have different:

- Loan conditions

- Interest rate

- Fees

- Approval process

Always look out deals.

4. Pre-approval

A pre-approval indicates sellers you are in good financial standing.

5. Provide the Documents

Lenders generally want:

- Proof of Income

- Returns for income tax

- Bank statement

- Job Description

6. Final Approval and Closing

When the paperwork is authorised it is signed and the ownership is transferred to the buyer.

Best Advice for Handling a Mortgage

A good mortgage may save you a lot of money in the long term.

Additional Payments

Paying more on your loan reduces the principle quicker and reduces the total interest you’ll pay.

Improve Your Credit Score

Better credit may assist later on refinancing.

Refinance at Lower Rates

Refinancing might help you cut your monthly payments or the length of the loan.

Set Up an Emergency Fund

You may not be able to make your payments due to unanticipated expenditures.

Many experts recommend saving 3 to 6 months of spending.

Steer Clear of Big Debts

Large loans or bills on your credit card might be bad for your financial wellness.

Avoid These Mortgage Mistakes

There are many blunders that borrowers make in the mortgage process that are entirely preventable.

Borrowing Too Much

Just because you were accepted for a lot doesn’t imply you should borrow all that money.

Hidden Costs Are Missing

Taxes, insurance and upkeep charges build up fast.

Selecting the Incorrect Loan Type

If interest rates rise, a variable-rate mortgage might be costly.

Loan Comparisons Not Included

When you don’t compare lenders it might mean paying thousands extra in interest.

Overdue Payments

Late payments might ruin your credit score and cost you more.

Best Mortgage Tools & Solutions

There are a number of tools available to assist consumers better manage their mortgages.

Mortgage Tools That Work

- Mortgage calculators

- Amortisation Calculator

- Interest comparison tools

- Refinancing calculator

- Budgeting applications

These tools allow you to estimate the following:

- Monthly payment

- Total Interest

- Repayment conditions

- Loan affordability

Mortgage Rate Comparison Chart

| Mortgage Type | Interest Rate | Monthly Payment | Stability | Risk Level | Best For |

|---|---|---|---|---|---|

| Fixed Rate Mortgage | Fixed | Stable | Yes | Low | Long term house owners |

| Variable Rate Mortgage | Changes Over Time | Unstable | No | Medium/High | Flexible borrowers |

| Interest-Only Mortgage | Lower at First | Temporary Low Payments | No | High | Short term purchasers |

| Government Backed Loan | Often Competitive | Stable | Yes | Low/Medium | First time buyers |

Conclusion

Understanding how mortgages operate is vital when you purchase a property. A mortgage is not simply a loan of money, it is a long-term financial commitment that will effect your future budget and lifestyle.

The key to becoming a successful homeowner is choosing the correct form of mortgage, researching around for the best lenders, understanding what fees are involved and being disciplined with repayments.

If you’re a first-time buyer in the US, UK or Europe, studying the fundamentals of mortgages can help you make better decisions and minimise financial hardship.

Do your homework, utilise mortgage calculators and get expert help if you need it.

If you liked our blog you can connect by our social profile :

Follow us for real estate tips, tools, and updates